Under the terms of the definitive agreement, Husky shareholders will receive 0.7845 of a Cenovus share plus 0.0651 of a Cenovus share purchase warrant in exchange for each Husky common share.

The shares of Cenovus Energy fell yesterday 8.4% to CAD 4.47 (attachment 3) and the shares of Husky Energy gained 12% to CAD 3.55 (attachment 4).

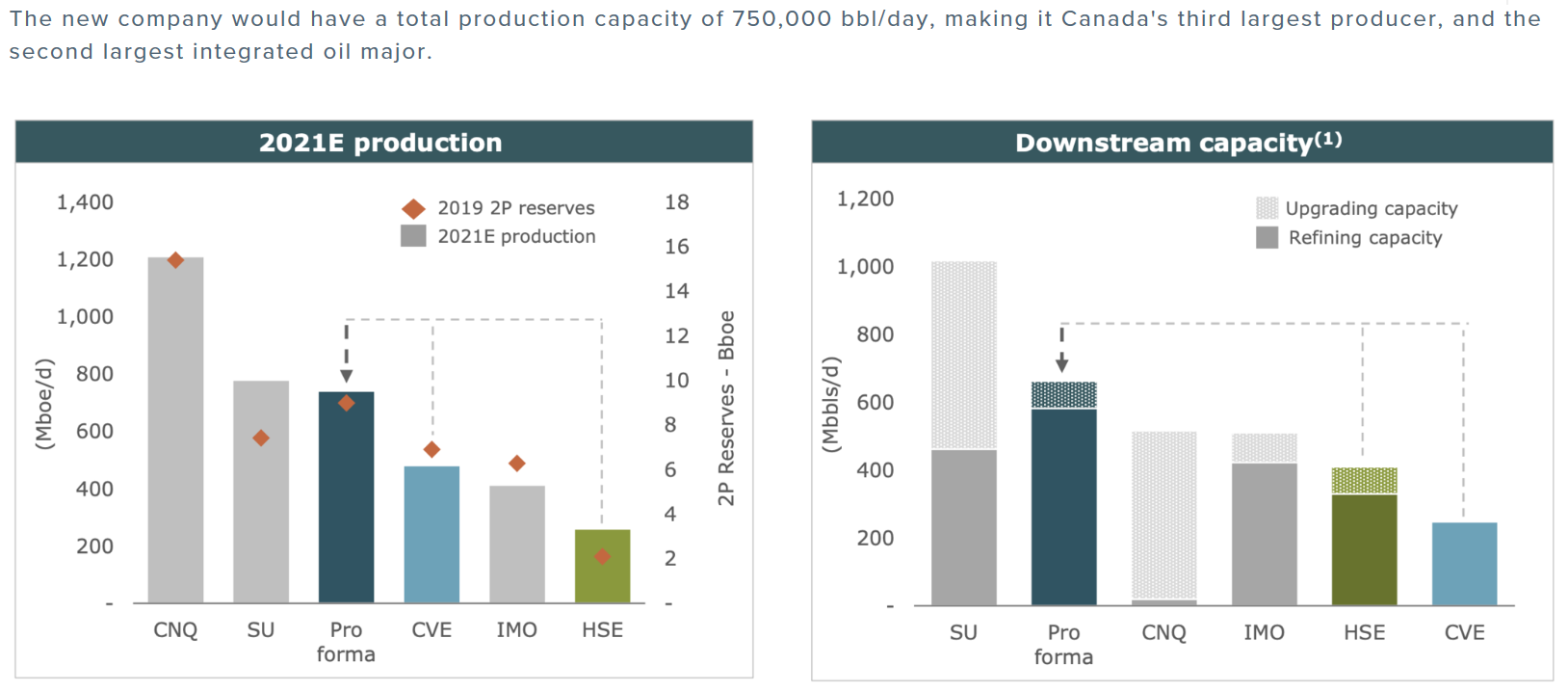

Buying Husky will boost Cenovus's production to about 750'000 barrels per day (b/d) from about 475'000 b/d of oil equivalent. It will gain substantial downstream assets, namely additional refinery and pipeline capacity. The Alberta Government will stop setting monthly oil production limits in December in a bid to create jobs and to use available pipeline capacity.

Cenovus' lack of refining and pipeline assets has been a major issue as Western Canadian Select (WCS) oil prices plummeted relative to West Texas Intermediate (WTI) prices.

WTI oil price trade currently at US$ 38.50 whereas Western Canadian Select prices at US$ 30.00 per barrel. Attachment 5 displays the oil prices (red-Western Canadian Select (WCS) - black West Texas Intermediate (WTI).

Attachment 6 shows the natural gas prices. The Canadian gas (AECO) is also selling at a discount to U.S. gas prices (Henry Hub).

The shares of Husky Energy have been in a strong downtrend for years as attachment 7 shows. The shares of Cenovus Energy also are in a steep downtrend (attachment 8).

Oil producers, pipeline shippers, and refineries are all struggling as there is too much oil coming out of the ground, with not nearly enough demand or places to store it.This resulted Canadian producers to sell their oil at hefty discounts to WTI, not only because of the heavier sour variety they are pumping out of the oil sands, but also because of limited pipeline capacity that moves the oil out of the Province of Alberta, the heart of the Canadian oil industry.

The Canadian ETF for oil and natural gas producing shares (XEG) CAD 4.26 shows there has been no joy to invest in Canadian oil and gas producers over the last few years (attachment 9).

We have been writing fore some time that we don't see oil prices entering into a bull market. There is very strong resistance between US$ 45 to US$ 50 per barrel (WTI prices) (Attachment 10). There is a huge amount of oil production capacity, which can come on stream if firmer oil prices persist over a shorter period of time.

No comments:

Post a Comment